When you walk out of an insurance office in California with a new policy, your final payment often includes a charge that surprises people: a broker fee. It's usually labeled something like "agency fee," "policy fee," or "processing fee." It is not the insurance premium. It's separate — and it goes directly to the broker, not the insurance carrier.

Broker fees in California typically range from $50 to $400 per policy, charged at new-business time and sometimes again at renewal. For a family with two cars, that's potentially $600-$800/year in fees on top of the actual insurance premium, going to the agency for paperwork the agency was going to do anyway.

What the California Department of Insurance says

Broker fees are legal in California. Licensed insurance brokers can charge them, as long as:

- The fee is disclosed in writing before you sign

- You sign a "broker fee agreement" acknowledging it

- The fee is reasonable for the services rendered

They are not mandated by the state. They are not part of the insurance premium the carrier requires. They are an extra charge the broker chooses to add.

Who charges broker fees in California?

Many of California's biggest non-standard auto insurance chains are known for charging substantial broker fees. A few of the most commonly cited:

- Freeway Insurance — charges a broker fee on most non-standard auto policies, which is one reason their advertised rates often look lower than their final out-the-door price

- Fiesta Auto Insurance — broker fees are standard across their California locations

- A number of smaller agencies that write SR-22, high-risk, and first-time driver policies also charge fees in the same range

This isn't illegal or shady — it's just how they've structured their business. The agency earns a commission from the carrier AND a fee from you. It means the customer pays twice for the same transaction.

Why do they charge broker fees?

Three reasons, honestly:

- Margin on high-risk policies is thin. When a carrier underwrites a high-risk driver (someone with a DUI, suspended license, or no prior insurance), the carrier's commission to the agency is smaller than on a standard policy. The broker fee closes that gap. This is also why drivers searching for cheap SR-22 insurance near me often see the lowest-quoted premium balloon at checkout — the fee is where the agency makes its money back on a thin policy.

- Advertised rates stay low. If the broker fee is listed separately, the quoted premium looks more competitive — even though the total out-the-door cost is higher.

- They can, and customers often accept it without questioning. Once you're in the office with your paperwork ready, most people don't want to start over.

What we do differently at Via Rapida Services

Via Rapida Services and our parent agency Insurance City do not charge broker fees on standard auto, home, or life insurance policies. Your total out-the-door price is the premium the carrier quoted — no surprise fees added on.

There are a few exceptions we want to be transparent about:

- Certain high-risk and specialty policies may carry a small service fee — we tell you before we write the policy, always in writing, and you can walk away

- DMV registration services and commercial specialty lines have their own separate service charges, which is standard industry-wide

The difference matters. On a standard auto policy at $1,800/year, a $300 broker fee at Freeway or Fiesta is effectively a 16% markup you're paying for no additional value. That's money that should stay in your pocket — or buy you a higher liability limit you actually benefit from. The same logic applies to specialty lines like cheap motorcycle insurance in California — a $200 broker fee on a $600/year motorcycle premium is a 33% markup, which is why it pays to ask for the out-the-door price before you sign.

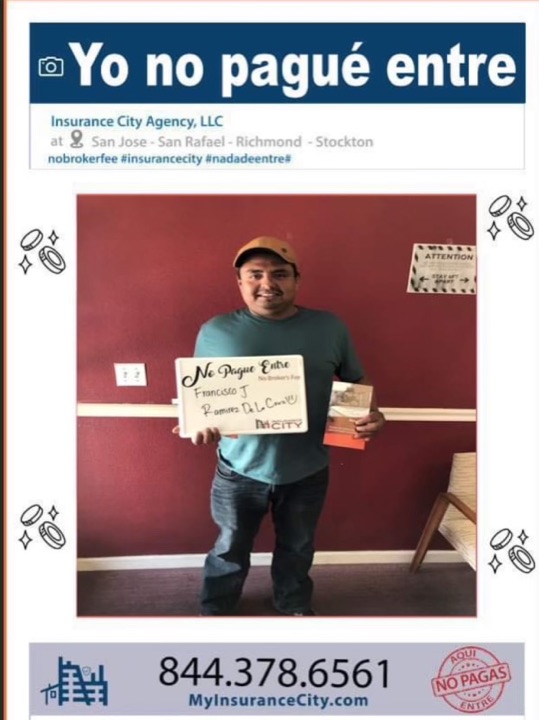

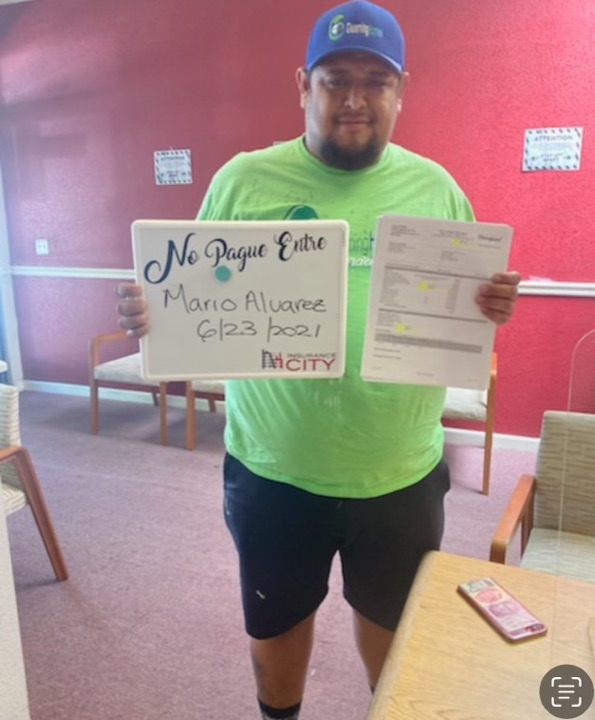

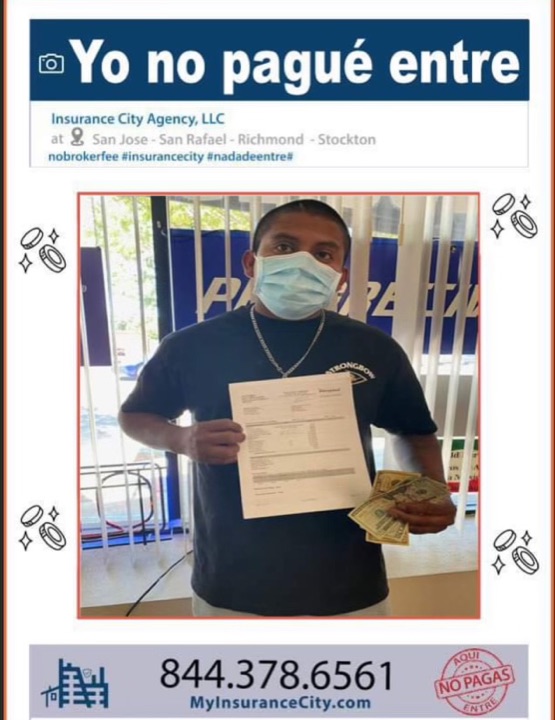

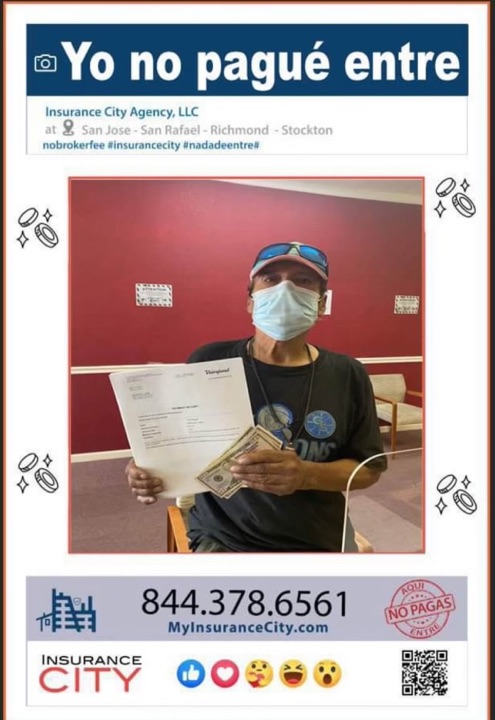

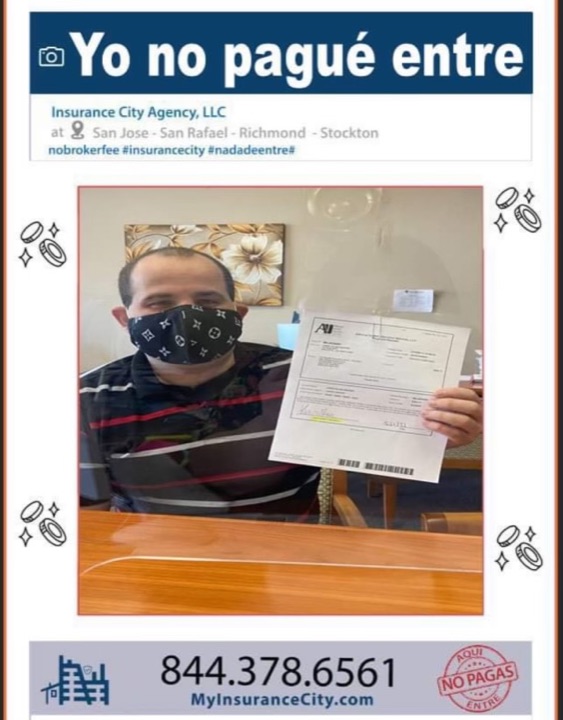

Real Insurance City customers — no broker fee paid

Photos taken in our offices when each policy was bound. Each customer holds the signed "No Pague Entre" / "No Broker Fee" card we give every standard policyholder.

10 of thousands of Insurance City policyholders. Photos taken in our Stockton office at the time of policy binding. Used with customer consent. Names omitted for privacy.

How to tell if you're paying a broker fee

Look at the paperwork from your current or last insurance purchase. Find the page titled Broker Fee Disclosure or Broker Fee Agreement. If you signed one, you paid one. The amount is listed right there. If you didn't sign one, you didn't.

You can also check your receipt: if the premium and the "agency fee" or "policy fee" are listed as separate line items, the agency fee is the broker fee. If there's only a premium charge, you didn't pay one.

What to do if you've been paying broker fees

You cannot get the fee refunded after the fact — you signed the disclosure. But at your next renewal, you have options:

- Shop around. Call us or another broker-fee-free agency and get a quote on the same coverage. If our total out-the-door price is lower than your current premium plus broker fee, switching saves you money.

- Negotiate with your current broker. Sometimes if you threaten to leave, they'll waive the renewal fee. This works less often than you'd hope, but it costs nothing to try.

- Switch at renewal. You are not locked in. California law allows you to change carriers at any time, with your new policy taking effect the same day. If you don't currently own a vehicle but still need to maintain coverage history (often the case after selling a car or moving), a non-owner car insurance policy in California is a low-cost way to keep continuous coverage and shop around without paying a renewal broker fee on a vehicle policy.

Frequently Asked Questions

Is a broker fee the same as the insurance premium?

No. The premium is what the insurance carrier charges for the coverage itself. The broker fee is an extra charge added by the agency on top of the premium. You can have a low premium AND a high broker fee.

Do all insurance agencies in California charge broker fees?

No. Some do, some don't. It's a business decision made by each agency. Freeway and Fiesta do. Via Rapida Services and Insurance City Agency don't, on standard policies.

Is there a legal maximum for broker fees in California?

Not by statute, but the California Department of Insurance can investigate fees they consider "excessive" or "unreasonable." In practice, most broker fees are in the $50-$400 range; fees above $500 on a standard policy are unusual.

Do broker fees apply to home insurance and business insurance too?

They can. Any type of policy written by a California insurance broker can carry a broker fee. Most of the noise is around auto insurance because that's where volume is highest.

How do I compare a quote from Via Rapida to a quote from Freeway or Fiesta?

Ask both agencies for the total out-the-door cost including any broker fees, policy fees, or processing fees. Don't compare the quoted premium alone. The real number is premium + all fees = what you pay today. The same comparison rule applies if you're shopping a specific carrier — for instance, when looking up National General insurance near me, the carrier's quoted premium and the broker's added fee are two different numbers, and only the combined total tells you what your monthly payment will actually be.

Get a true out-the-door quote

Call us at 209-670-1556 or walk into one of our three California offices (Stockton, San Jose, San Rafael). We'll give you the total out-the-door price upfront, in writing, no broker fees on standard policies, and show you exactly how it compares to what you're paying today. See our full comparison of Via Rapida vs. the big chains.